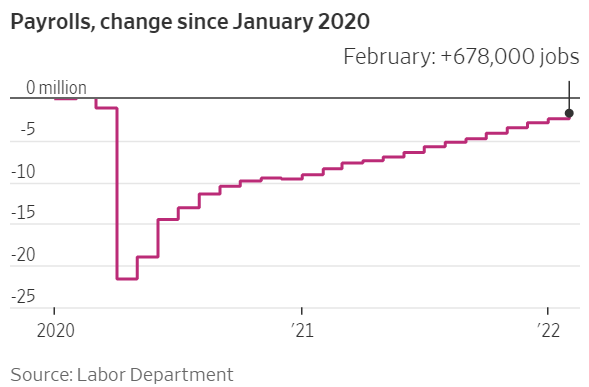

U.S. Economy Added 379,000 Jobs in February

The labor market continued to heal in February as the U.S. economy added 379,000 jobs, easily beating the consensus expectation of 200,000 jobs. A particular bright spot within the February employment report was the 355,000 gain in jobs at leisure & hospitality businesses, which shows the waning effects of COVID-19. Given the weather effects in February, the ongoing rollout of the vaccine, and government stimulus programs, look for even faster overall job growth in March.

Why it matters: An increase in jobs translates into greater spending power for consumers and therefore a healthier, faster growing, economy. Greater spending power equates to higher levels of consumption – the backbone of the U.S. economy as consumption accounts for approximately 2/3rds of economic growth.